- World’s 2nd Largest Art Museum Going NFT - July 30, 2021

- Finance a Film via Blockchain - July 1, 2021

- 40% of New Fintech Firms in Hong Kong Use Blockchain - June 8, 2020

How cryptocurencies are ever going to be accepted by the masses as a means of payment or trade is anyone’s guess. Bitcoin started off with the idea of becoming the defacto digital currency of the world, but after 11 years being introduced to the world, there are still some reluctance by many quarters. Business Insider has broken the main factors of how and what truly affects cryptocurrencies mass adoption.

Cryptocurrencies and blockchain have been around for a long time, but within the past decade they’ve propelled into mainstream acceptance and adoption — as not only alternative forms of payment for individuals but also time and cost savings for a multitude of enterprise applications.

After the launch and success of cryptos like Bitcoin, Litecoin, Ethereum, and more, other cryptocurrencies soon followed — hundreds, in fact. The technology isn’t merely limited to fintechs either; legacy financial services firms, such as Goldman Sachs and JPMorgan, and tech giants like Facebook have taken notice and begun developing their own cryptocurrencies in-house.

Today, there are nearly 2,500 cryptocurrencies worth more than $252.5 trillion trading in the market. The price of cryptocurrencies ranges between approximately a quarter to thousands of dollars, though the exact price tags fluctuate every day.

After hitting its all-time high of nearly $20,000 in December 2017, Bitcoin has been notoriously volatile over the last few years, leaving many investors skeptical. However, it appeared to make a comeback in 2019, doubling in value throughout the course of the year and ultimately spiking in November. Though some doubts remain, the upward trend re-validated the crypto king as a high-growth asset class for many.

And while Bitcoin and other major cryptos have been legitimized in recent years through their representation on top online trading brokers such as Schwab, E-Trade, TD Ameritrade, and CoinBase, this isn’t necessarily true for all blockchain applications.

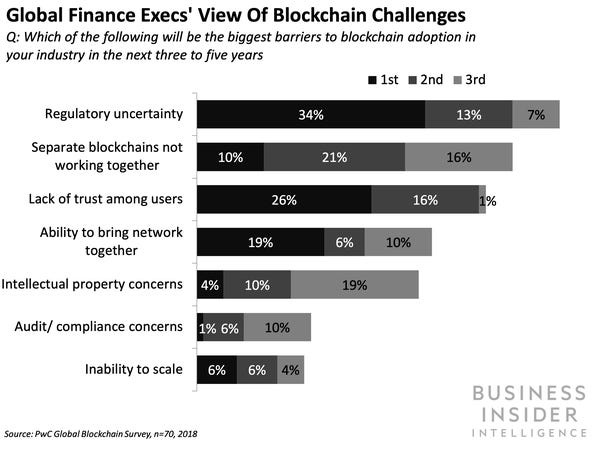

Along with turning heads of businesses, financial institutions, and governments all around the world, the technology’s decentralized nature is raising regulatory concerns and questions. Most notably, Facebook’s proposed blockchain cryptocurrency, Libra, and its digital wallet, Calibra, have been entrenched in heated public battles with lawmakers ever since their announcement in June, 2019.

After its unveiling, Libra was immediately called into question by the U.S. Senate, resulting in dozens of letters from lawmakers over “risks the project poses to consumers, regulated financial institutions, and the global financial system.” Worse, major partners including PayPal, eBay, Mastercard, Strip, Visa, subsequently withdrew from The Libra Association — all before anything even launched.

It might not be the Wild West anymore, but the regulatory landscape for crypto and blockchain is still rocky at best. In this article, Business Insider Intelligence, explores how regulations are adapting to the spread of these technologies, and the impact they’re having on its adoption.

Digital Asset Regulations All Over the World

Cryptocurrency has been a topic of continual debate among global economies and governments. While some administrations maintain a generally Bitcoin-friendly stance, issuing guidance to support its use, others remain undecided, having yet to put forth any official decisions on legality or acceptance.

Still, some governments feel that allowing cryptocurrency would ultimately result in loss of economic power and a shift towards decentralized economies globally. A handful of countries including China, Russia, and Colombia have even banned Bitcoin and other cryptocurrencies, outlawing their use and investment altogether.

Business Insider Intelligence has gone into further depth in identifying some of the key blockchain regulations and associated issues in the U.S., Europe, and the rest of the world.

Blockchain Regulations in the U.S.

The U.S. maintains a generally positive outlook on the use of Bitcoin and other cryptocurrencies, though few formal rules have actually been introduced. Most of the regulatory discussion surrounding blockchain has been at the agency level, including the Department of Treasury, Securities and Exchange Commission (SEC), Federal Trade Commission (FTC), Internal Revenue Service (IRS) and Financial Crimes Enforcement Network (FinCEN) — all of which hold differ in their definitions of “cryptocurrency,” as well as their stances on how regulation should be applied.

While FinCEN does not consider cryptocurrency to be legal tender, it does consider exchanges as money transmitters subject to their jurisdiction. Meanwhile, the IRS has begun considering cryptocurrencies property, and has issued tax guidance accordingly.

Despite interest from these agencies, the federal government has not exercised its constitutional preemptive power to regulate blockchain to the exclusion of states (as it generally does with financial regulation), thereby leaving individual states free to introduce their own rules and regulations.

In June 2015, New York became the first state in the U.S. to regulate virtual currency companies through state agency rulemaking. As of 2019, 32 states have introduced legislation accepting or promoting the use of Bitcoin and blockchain distributed ledger technology (DLT), while a few have already passed them into law. Some of these states have also established task forces to study the technology’s use further.

Bitcoin took a major step in 2017, when it was granted the same financial safeguards as traditional assets. The FTC gave cryptocurrency trading platform operator LedgerX approval to become the first federally regulated digital currency options exchange and clearinghouse in the U.S.

Additionally, in June 2019, SEC-registered clearing and execution company Apex Clearing launched a trading platform for brokers-dealers and financial advisors to help their clients trade the four major cryptocurrencies – Bitcoin, Bitcoin cash, Ethereum, and Litecoin – through its subsidiary Apex Crypto.

See the full list of U.S. state-by-state legislation for blockchain and cryptocurrency here.

Blockchain Regulations in Europe

The overall approach of the European Union (EU) towards blockchain technology has been positive and welcoming — but only recently did it put forth official legislation to regulate it. On January 10, 2020, the EU signed its 5th Anti-Money Laundering Directive (5AMLD) into law, marking the first time that cryptocurrencies and crypto services providers will fall under regulatory scrutiny.

According to the EU’s 5AMLD fact sheet, as part of an effort to fight money laundering and terrorist financing, the law increases transparency around the owners of virtual currencies. It proposes that the EU’s member states create central databases comprised of crypto users’ identities and custodian wallet addresses for Financial Intelligence Units (FIUs) to access.

Now that they fall under the same regulatory requirements as banks and other financial institutions, any crypto service providers in charge of holding, storing and transferring virtual currencies must register with financial authorities, including identifying their customers and reporting any suspicious activity to FIUs.

Many EU member states have been preparing for the 5AMLD deadline for some time; Finland, the Netherlands, Germany, Austria, and France have all either begun transposing elements of the new directive into national law or already implemented comprehensive controls.

In the UK, where then Brexit transition period looms for the remainder of 2020, the UK Financial Conduct Authority (FCA) has become the anti-money laundering (AML) and counter-terrorist financing (CTF) supervisor of the country’s crypto-asset activities, stating that crypto exchanges, ATMs, peer-to-peer platforms, custodian wallet providers, and token issuers all must comply with its rules.

These actions are precursors to a more unified approach; in February 2020, the chair of the Switzerland-based Financial Stability Board (FSB) stated that financial regulators must speed up the process of developing a comprehensive regulatory framework for cryptocurrencies. The letter, addressed to finance ministers and G20 central banks, called for global regulators to act now – particularly to look at the risks and benefits of stablecoins – to keep up with the rapid pace of innovation and change in the crypto market to avoid losing control of it.

Regulating Blockchain Technology Worldwide

Though Bitcoin tends to get the most hype, blockchain, the underlying DLT powering the virtual currency, has a much broader range of use cases. In fact, blockchain has found a home in nearly every industry, from financial services and payments to healthcare, energy, and property (even intellectual property) management. And many legacy institutions are now finding themselves challenged by tech-savvy upstarts proposing blockchain-based solutions.

But despite its increasingly prevalent use among businesses and consumers, blockchain is still a nascent technology when it comes to regulation. Around the globe, as within the US, no consistent policy has yet evolved. Rather, countries have been left to their own discretion — with some, like those in Europe transposing regulation into their national laws, and others shunning the technology altogether.

The grey area is vast, as many countries are trying to balance building a society that fosters innovation and entrepreneurship with one that protects its citizens from crime, fraud, and other harm.

To provide more detail on specific actions taken by local jurisdictions, Global Legal Insights published a 2019 report outlining the current regulatory framework by country.

As blockchain and cryptocurrency become more prevalent in the private sector and among consumers, governments globally are learning how to implement regulations across industries. Business Insider Intelligence has taken a closer look at the technology’s use within financial services in the Blockchain in Banking report.

This research report explores blockchain successes and failures at major banks and outlines steps other players can take to find success in their own blockchain projects.

- This is a preview of the Blockchain in Banking research report from Business Insider Intelligence.

- Purchase this report.

- Business Insider Intelligence offers even more insights like this with our brand new Banking coverage. Subscribe today to receive industry-changing banking news and analysis to your inbox.

Disclaimer: Blockchain Academy Malaysia and/or its blog editors do not receive any commission or contributions if you were to purchase any products/services or reports from Business Insider.